You may already have a strong product and a growing presence on Amazon, but scaling that success often comes down to one key factor—access to capital. For many sellers, securing funds quickly can be a real hurdle. Growth opportunities don’t wait, and neither should your funding. You can do it by Amazon lending.

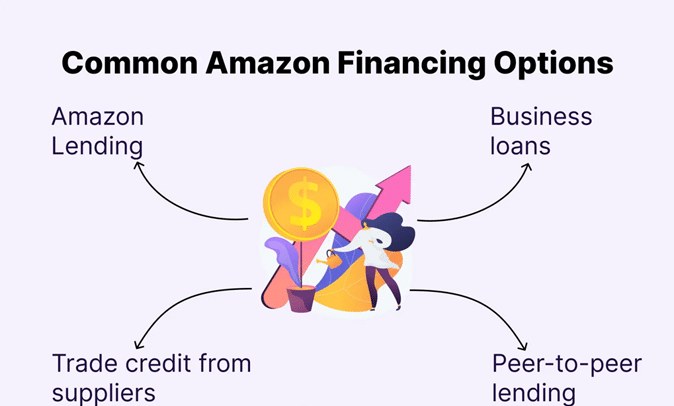

With multiple financing routes available—ranging from Amazon’s own lending program to inventory financing, factoring, and traditional bank loans—it can feel overwhelming to choose the right path. In this article, we’ll break down Amazon Lending and inventory financing so you can decide which suits your business best.

Amazon Lending

Amazon Lending is a funding program designed specifically for marketplace sellers. It provides short-term loans to eligible businesses, helping them purchase inventory and continue selling on Amazon. Loan amounts typically range from $1,000 to $750,000, but access to the program is strictly by invitation.

Since eligibility is limited, detailed information about loan limits, fees, and repayment terms isn’t always publicly available. This can make it difficult for sellers to predict exactly what kind of offer they might receive.

How Amazon Lending Works

If you receive an invitation, it’s important to understand how this financing option operates. Unlike traditional small business loans, Amazon Lending has a structure that aligns closely with your seller account activity.

In many ways, it resembles a merchant cash advance. You receive the funds upfront, and repayments are automatically deducted from your Amazon sales. This setup simplifies repayment and reduces the risk of missing due dates.

However, if your sales don’t generate enough funds to cover the payment, Amazon will charge the backup payment method linked to your account. This ensures they still receive their repayment regardless of your sales performance.

Amazon Lending vs Merchant Cash Advances

Although Amazon Lending shares similarities with merchant cash advances, there is a key distinction. With most MCA providers, repayment fluctuates based on your sales volume—lower sales mean smaller payments, and higher sales increase your repayment amount.

Amazon, on the other hand, follows a more fixed structure. A predetermined portion is deducted from your account regularly until the loan is fully repaid, regardless of whether your sales rise or fall.

This difference is especially important for sellers dealing with seasonal products, where revenue can vary significantly throughout the year.

Funding Speed and Process

One of the biggest advantages of Amazon Lending is how quickly funds become available. In some cases, sellers can receive approval within 24 hours. Once approved, the loan amount is deposited directly into your Amazon seller account, allowing you to reinvest in inventory almost immediately.

Advantages of Amazon Lending

Simple Application Process

Amazon streamlines the process by pre-selecting sellers who qualify for funding. If you’re eligible, you’ll receive an invitation through Seller Central and email. From there, you can accept the offer, decline it, or adjust the loan amount within the approved range—all within a few clicks.

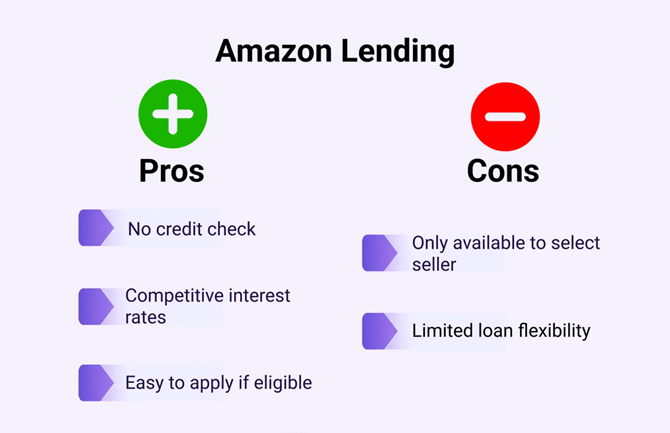

No Credit Checks Required

Unlike traditional lenders, Amazon does not rely on your credit score to determine eligibility. Instead, it evaluates your seller performance and account history. This makes it an appealing option for sellers who may not meet the strict requirements of banks or other lenders.

Competitive Interest Rates

Interest rates for Amazon loans are relatively reasonable compared to other short-term financing options. Rates can go up to around 16% for a 12-month term, which is generally lower than many merchant cash advance providers.